Click here for the new Anchor Rising & Ocean State Current page

Click here for the new Anchor Rising & Ocean State Current page

Budgeting for a Sequester, by Carroll Andrew Morse

Fiscal Policy

1:39 PM, 02/28/13

The Governor's 2014 Budget for Rhode Island in Historical Perspective, by Carroll Andrew Morse

Fiscal Policy

3:00 PM, 01/17/13

The Unmentionable Solution to the Fiscal Cliff, by Justin Katz

Under the Government's Wing

7:30 AM, 11/27/12

Sequestration Cuts....aren't, by Marc Comtois

Fiscal Policy

9:00 AM, 09/15/12

Rhode Island's Decidedly Non-Austere State Budget History: (Third and Final Update), by Carroll Andrew Morse

Fiscal Policy

4:30 PM, 06/ 7/12

Ted Nesi's Interview with David Skeel on the Basics of Municipal Debt, by Carroll Andrew Morse

Fiscal Policy

3:00 PM, 03/ 2/12

Balanced Budget Amendment Coming up For a Vote in Congress, by Carroll Andrew Morse

Fiscal Policy

1:45 PM, 11/17/11

Claiborne Pell Was a Fiscal Extremist, According to Today's Democrats -- He Supported a Balanced Budget Constitutional Amendment, by Carroll Andrew Morse

Democrats on the March

8:00 AM, 11/ 7/11

Walter Russell Mead on Rhode Island as Athens on the Pawtuxet, by Carroll Andrew Morse

Fiscal Policy

11:30 AM, 10/24/11

Even if it's Amazing, It's not fair, so I hate everything, by Marc Comtois

On a Lighter Note...

10:04 AM, 10/10/11

February 28, 2013

Budgeting for a Sequester

Numbers between $17M and $25M are being reported as the cost of the sequester to Rhode Island state government spending. However, if a few state departments did nothing more than stay within their original FY2013 budgets, and the funding tentatively intended for their overruns could be intelligently redirected, the impact would only be about half of that amount.

Let's begin by noting that, for the most part, the various departments of RI government are exhibiting a reasonable degree of budgetary discipline. In other words, according to the Governor's proposed budget document for FY2014, most departments won't spend more than they were appropriated for FY2013 (in Rhode Island, we take our fiscal successes wherever we can find them).

However, at least one government department is an exception to this: the General Assembly. The Rhode Island General Assembly was appropriated $37.2M from the state's general revenues for fiscal year FY2013, a 10.5% increase over the previous year. In the Governor's revised budget for FY2013, the GA is appropriated $40.4M from general revenues, an overrun of $3.2M (8.6% more than their appropriated amount). If the state legislature does nothing more than stay within its original FY2013 appropriation (this is not a cut; they still get their 10.5% increase over the previous year), it would free up $3.2M to be spent on areas impacted by the sequester. Since the money saved would all come from general revenues, the legislature could pretty much spend it wherever it wanted to (just like it could choose to spend on itself, while other programs are being impacted).

The Information Technology section within the state's Department of Administration also spends more, according to the Governor's revised FY2013 budget, than it was allocated in the original. The revised budget allocates an extra $930K from general revenues to finish the year. However, it should be noted that DoA Information Technology (unlike the General Assembly) was budgeted very conservatively at the start, with FY2013 costs for personnel and operating expenses initially budgeted for about $1.8M less than the previous year. Maintaining their general revenue at its original FY2013 level still leaves 3% more for personnel and operations than originally appropriated.

The last area of noticeable budget increase is one of the largest, though it is not under state government control alone. This area also reveals something about priorities in government budgeting. As you may have heard, the executive branch of Rhode Island government is planning to set up an Obamacare "Health Benefits Exchange". In the original FY2013 Rhode Island budget, $22.2M was allocated for initial set-up expenses, all paid for with Federal dollars. In the Governor's revised budget, the cost of setting up a Healthcare Benefits Exchange jumps by 30% to $28.8M, still all from Federal funding. If costs were limited to their original FY2013 budget amount (and, once again, being asked to stay within an approved budget is not a cut), it could free up about $6.6M to be applied to other human service programs. 98% of Health Benefits Exchange spending in FY2013 is on "personnel", so no assistance program would be adversely affected, and the salary-spending plans from the Governor's "revised" budget could be resumed just 3 months from now, on June 1, at the start of the new fiscal year.

Asking these 3 programs to stay within their budgets for this year could free up about $10.8M to replace sequestered monies. That leaves a gap of somewhere in the vicinity of $6.2M to $14.2M to be closed (down from the original $17M to $25M).

Federal dollars allocated to Rhode Island state government, minus two programs 1) the Health Benefits Exchange, already accounted for above and 2) support for the Department Labor and Training, which was temporary and is in the process of being phased out, was $2.39B in FY2012. In the Governor's revised budget for FY2013 (which we'll assume doesn't include the sequester), that amount increases by $140M, to $2.53B. If we pick the larger of the sequester estimates and don't include DLT or Health Benefit Exchange programs, in conjunction with the three proposals suggested above, the rest of Rhode Island government would have to adjust to the sequester by spending "only" $125M more in Federal dollars than they did last year

Or, if it is decided that General Assembly spending on itself and that spending on healthcare bureaucratic cost overruns is more important than everything else, the sequester would mean that Rhode Island only gets to spend about $115M more in non-Health Benefits Exchange, non-DLT Federal dollars than it did last year. Hmmmm. Maybe I buried the lede on this one.

Anyway, with competent fiscal management, managing the "austerity" of a $115M budget increase should be feasible. We'll see how how well Rhode Island is able to handle it.

January 17, 2013

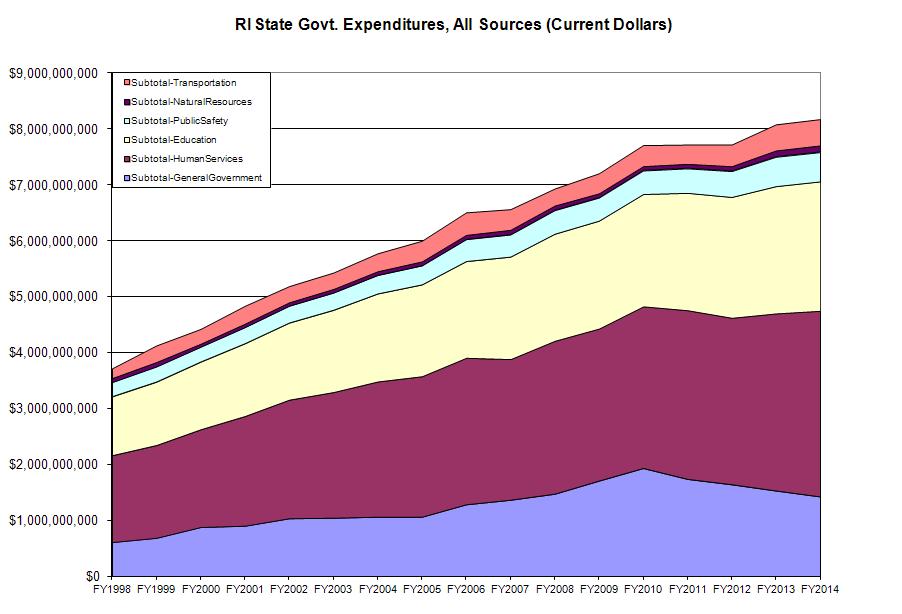

The Governor's 2014 Budget for Rhode Island in Historical Perspective

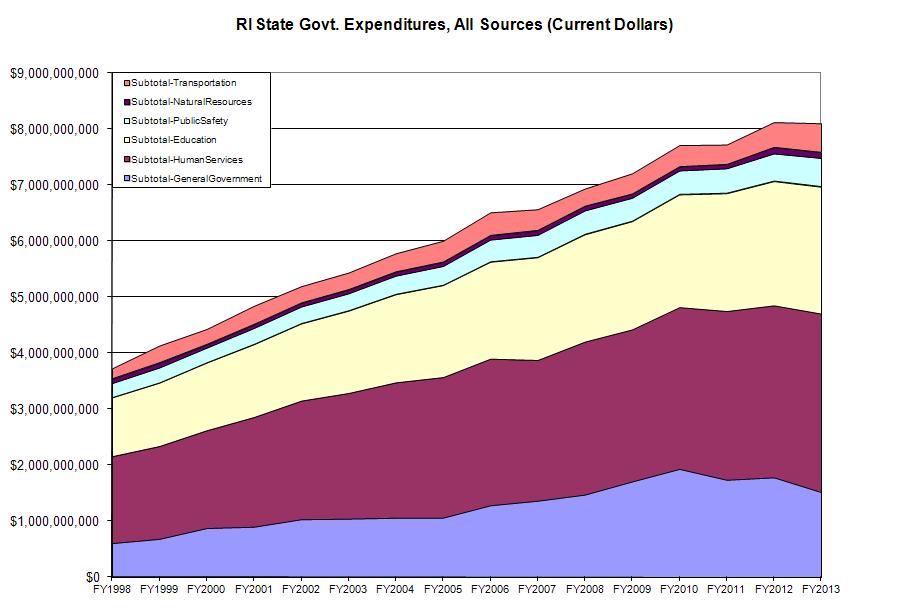

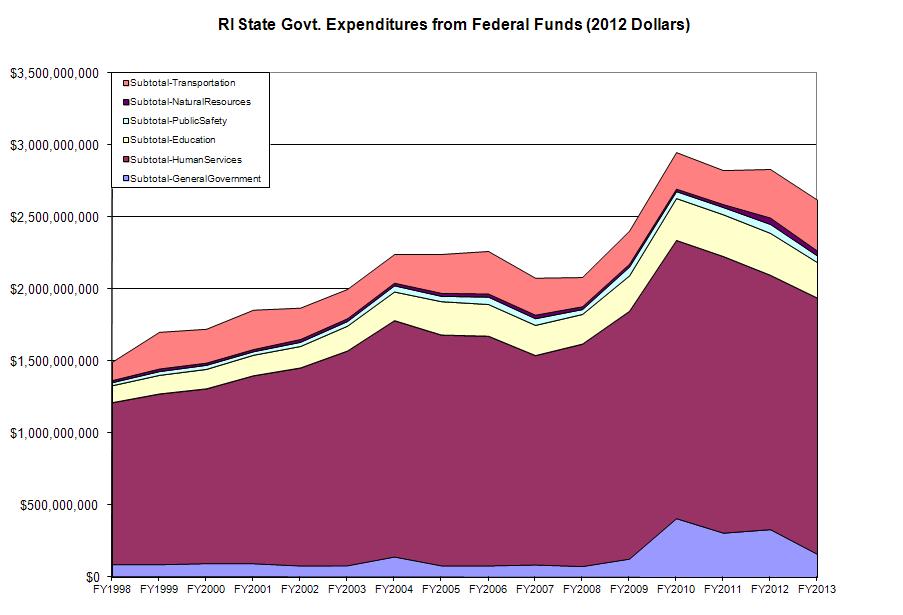

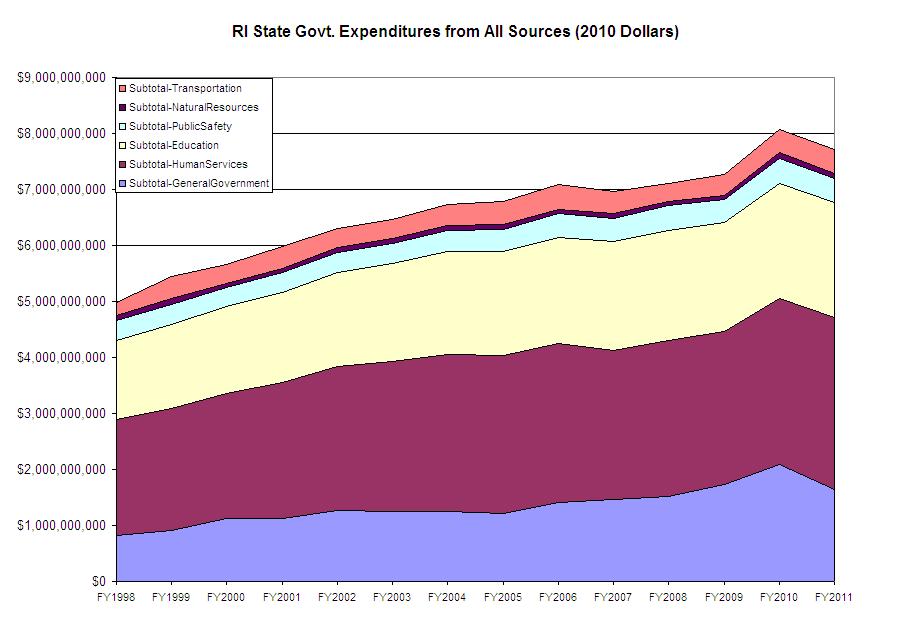

Here is the recent history of Rhode Island state government expenditures updated to reflect the Governor's proposed budget for 2014, made possible in part by the fast work done by the State of Rhode Island Budget Office to make the complete budget available on the ri.gov website.

As always, actual dollar amounts spent (or, in the cases of FY2013 and FY2014, to be spent) are presented first.

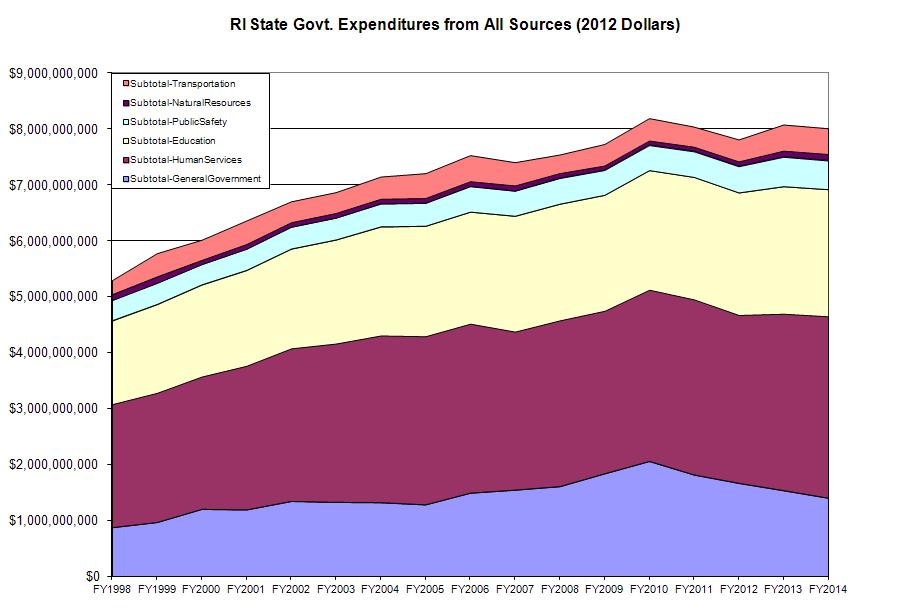

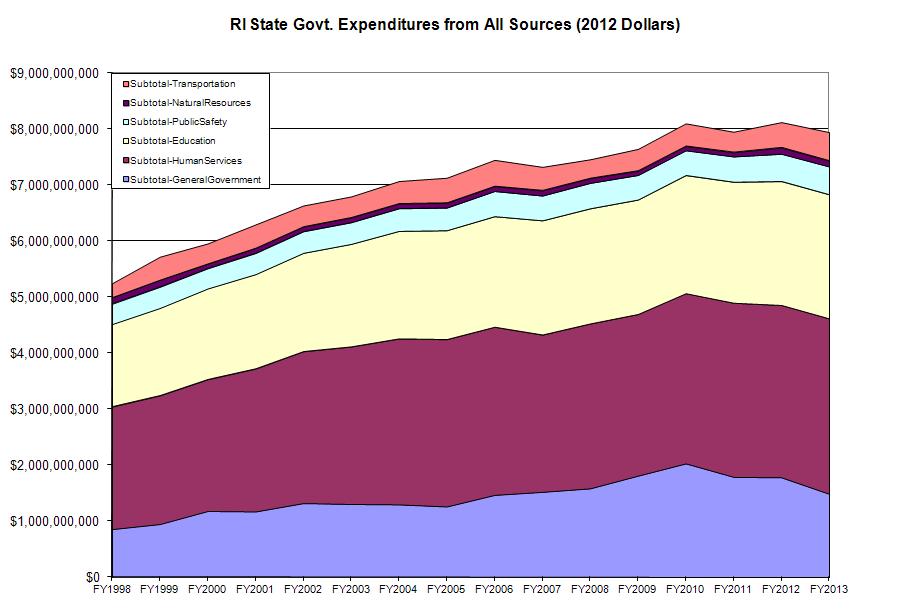

The next chart takes the spending amounts from all sources and adjusts them for inflation, based on data available from the Department of Labor and Training (and with 2% inflation is assumed for next year). The most distinctive feature of this chart is that FY2014 potentially represents a fourth consecutive year where state expenditures will be relatively stable relative to inflation, following more than a decade of nearly linear, year-by-year spending growth.

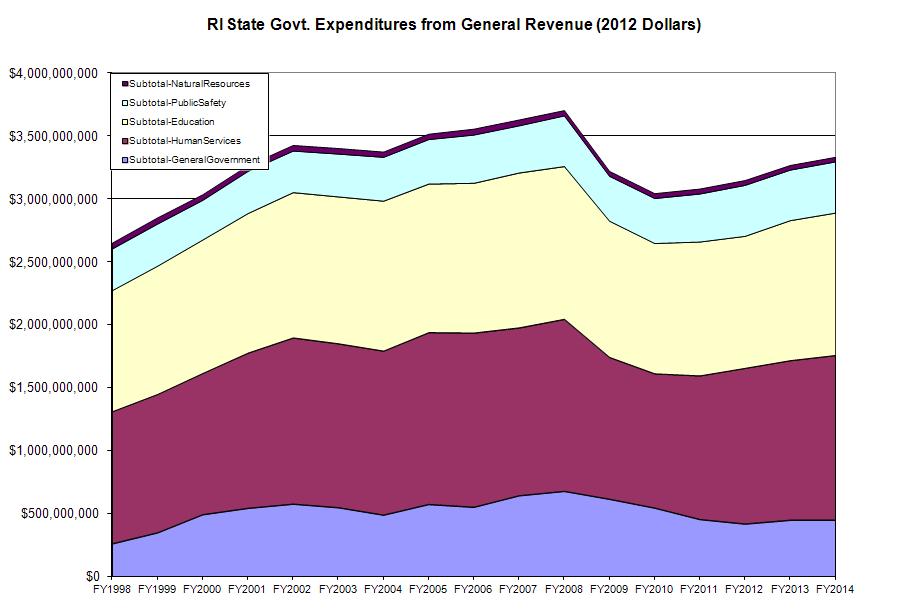

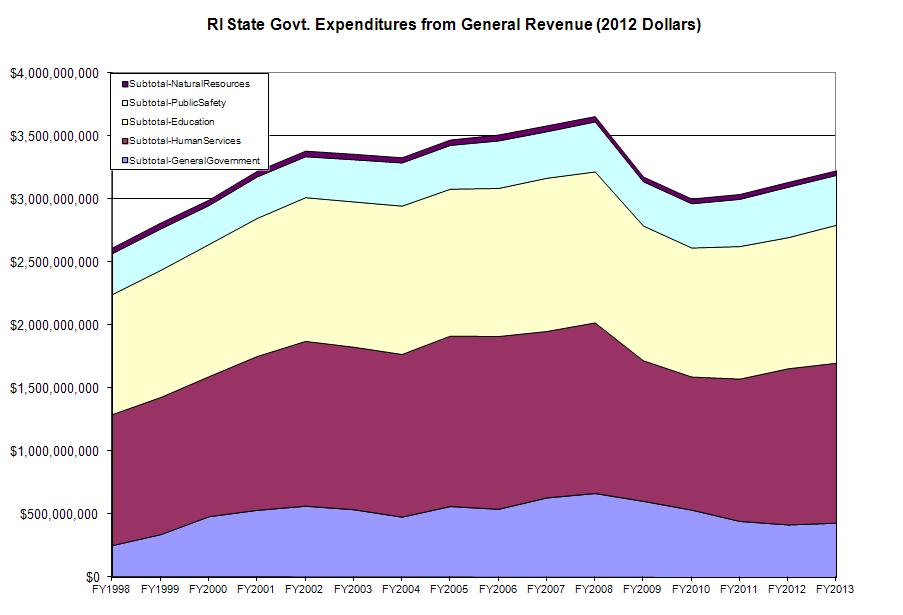

The amount of state government funded by general revenues (basically state taxes) does continue to grow in the Governor's proposed budget. If the totals in the Governor's proposed FY2014 budget are ultimately outlaid, Rhode Island general revenue spending will have grown by about 2.5% per year faster than inflation over the first three years of the Chafee administration.

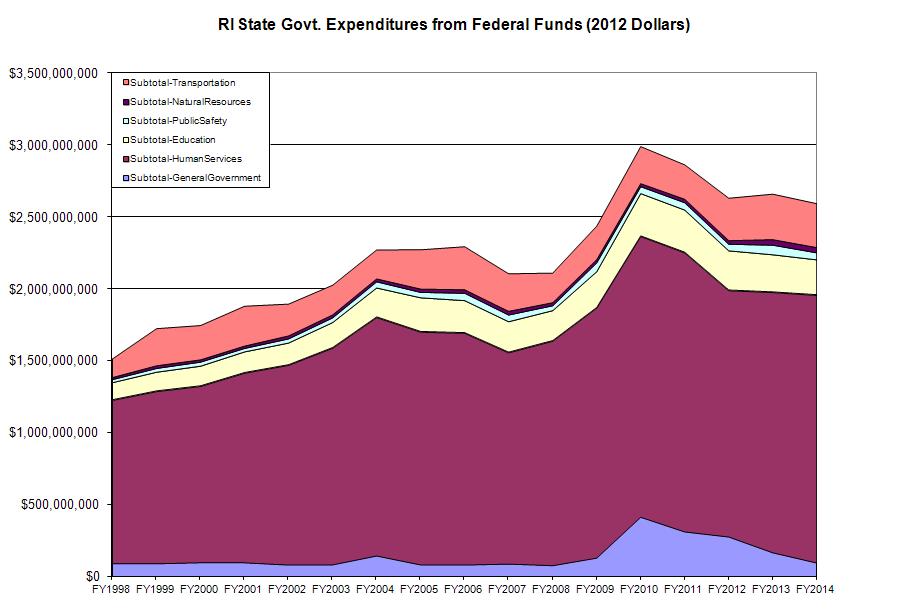

The last chart shows the Rhode Island state budget's Federal funding. The spike in "General Government" that occurred in FY2010 that has been gradually drawn down since then falls largely under the heading of grants and assistance offered by the Department of Labor and Training -- presumably unemployment insurance related. It is interesting to note that increased spending under "human services" makes up much of the difference this fiscal year and next.

November 27, 2012

The Unmentionable Solution to the Fiscal Cliff

Watch public policy even for a short while and the trick becomes evident. Whether we're talking my hometown of Tiverton, Rhode Island, (population 15,780) or the federal government, the maneuver is to claim increasing amounts of power and make sure that's the one thing not on the table when something has to give.

Thus, we get massive government interwoven like a terrible tumor around the vital organs of our economy. When the predictable illness follows, the two operations suggested, as if in opposition, are cuts on the spending side and increases on the revenue side.

Either, we're told, is apt to drive the patient into shock. The government can take money out of the economy through taxes, or it can stop putting money into the economy via cuts. That's not much of a choice.

September 15, 2012

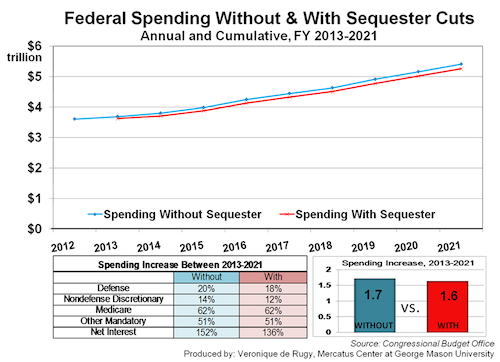

Sequestration Cuts....aren't

Veronique de Rugy (h/t) explains the supposed "cuts" in sequestration:

The sequester is an automatic budget enforcement mechanism triggered when the Joint Select Committee on Deficit Reduction fails to enact legislation to reduce the deficit by $1.2 trillion over the sequestration period. Instead of simply passing appropriated funds to the agencies, the U.S. Treasury “sequesters” the difference between the cap set in the BCA and the amount appropriated.So don't believe the hype from government, contractors or others. There will still be more borrowed money for everyone. Ain't that just great?Changes in spending from sequestration result in new budget projections below the CBO’s baseline projection of spending based on current law. The federal government would spend $3.62 trillion in the first year with sequestration versus the $3.69 trillion projected by CBO. By 2021, the government would spend $5.26 trillion versus the $5.41 trillion projected. Overall, without a sequester, federal spending would increase $1.7 trillion (blue line). With a sequester, federal spending would increase by $1.6 trillion (red line).

While the sequester projections are nominal spending increases, most budget plans count them as cuts. Referring to decreases in the rate of growth of spending as “cuts” influences public perceptions about the budget. When the public hears “cut,” it thinks that spending has been significantly reduced below current levels, not that spending has increased. Thus, calling a reduced growth rate of projected spending a “cut” leads to confusion, a growing deficit, and an ever-larger burden for future generations.

June 7, 2012

Rhode Island's Decidedly Non-Austere State Budget History: (Third and Final Update)

As the state budget goes before the full Rhode Island House today, here are a few graphics showing how this year's spending fits into the longer-term pattern of Rhode Island state spending. This first graph shows a slight breather, in terms of current dollars, in the continuing growth in state budgets that has been occurring for over a decade. ("Current dollars" is the formal economics term for amounts spent at the time they were spent, e.g. when your grandparents you that the newspaper only used to cost a nickel, they are telling you what the price of a newspaper was in current dollars).

One point however, related to the recent news about layoffs at the Department of Labor and Training: If you examine the DLT budget, you will find its Federal funding dropping $112M between this fiscal year and next, from about $224M to $112M -- following a jump up from about $70M to $330M between fiscal years 2009 and 2010. So in terms of current dollars, all of the "austerity" in this year's budget could be accounted for by reductions in Federal dollars that were known to be temporary from the beginning.

Chart 1:

Chart 2:

Using inflation numbers published by the Department of Labor and Training, spending totals from the past can be expressed in terms of "2012 dollars" (I assumed 2% inflation between this year and next year, for which there is no definitive data available, since it hasn't happened yet). The inflation adjusted totals show the continuation of a pause in the growth of inflation adjusted spending that began in FY2011, if this budget is held to(*), which follows $2 billion in spending growth above the level of inflation that had occurred over the previous decade. Calling this year's budget an "austerity" budget assumes that automatic faster-than-inflation growth in government spending is the norm.

(*) The state actually overshot its originally passed FY2012 budget by about $400M, though a large portion of that came from Federal money, and none was attributed to the state's general revenues.

Chart 3:

The next graph shows the inflation adjusted Rhode Island government spending from general revenues (basically state taxes). The first budget approved during the Chafee administration grew spending by about 3%, adjusted for inflation, relative to the final budget approved during the Carcieri administration.

And if inflation over the next year is in the 2%-3% range, the growth of spending adjusted for inflation will also be in the 2%-3% range (or, more properly, in the 3%-2% range). In terms of current dollars, general revenue spending is budgeted to grow by about $150M next year, or 5% relative to this year, as part of the some-call-it-"austerity" plan.

Chart 4:

The final chart presented in this post shows the Federal dollars included in the Rhode Island budget. Notable features on this chart are the spike resulting from the financial meltdown and associated stimulus, and a suggestion of what a future normal level of Federal spending might look like.

Figures compiled from data available from:

- The Rhode Island House of Representatives Fiscal Staff report on the FY2013 RI Budget.

- Previous year's gubernatorial budgets, archived by the RI Dept. of Administration's Budget Office.

March 2, 2012

Ted Nesi's Interview with David Skeel on the Basics of Municipal Debt

3 points about Ted Nesi's WPRI-TV (CBS 12) interview with University of Pennsylvania Law Professor and bankruptcy expert David Skeel are worth immediately noting:

- In the first half of the interview, Prof. Skeel advances that same argument, based on current law, that we at Anchor Rising have been making from a wider historical perspective for a while now -- government has no inherent authority to make promises to trade away that which it does not possess...

DS: The question is if a city or a state makes a pension promise, but does not fund the promises – which has been true in many states in recent years – what exactly is protected in the event of a default or of bankruptcy? A lot of people assume that what’s protected is the full promise, even if there’s no funding behind it.

This portion of the discussion should be of particular interest to those who want to invoke the "police power" as being central to the solution to Rhode Island's government-financing crisis. In particular, a strong case can be made that the future is best served not by expanding the police power to new circumstances, but instead by enforcing the proper limits on the government's appropriations power, an idea implicit in Prof. Skeel's argument, i.e. the government cannot legitimately promise everything because it does not own everything.Although this is certainly not free from doubt – this is unchartered territory in many respects – my view is that there’s a good argument that what’s protected is the amount of money that’s been set aside. Pension obligations are a form of what we refer to in the law as a property right, and other kinds of property rights are protected up to the value of the property that’s set aside for them. So if somebody has collateral for a transaction, we treat that promise as sacrosanct up to the value of the collateral.

- Towards the end of the interview, Prof. Skeel explains that one possible first-cut common-sense response to the idea of a bond default -- if there's a real price to risk, then bondholders should understand that there's a real possibility of not getting every payment -- is essentially correct...

TN: The argument I always hear back here is that Rhode Island governments can’t operate without being able to borrow money, and that without this protection we could be cut off from the bond markets. What do you make of that argument?

DS: I disagree with the assumptions underlying the argument, which is that if you don’t completely protect bondholders all possibility of borrowing will disappear. I just don’t think there’s evidence of that. The bond market view tends to be if you do anything that prevents us from getting 100 cents on the dollar, the world is going to come to an end. And my view is, there’s just no evidence of that. The evidence is really to the contrary – healthy municipalities will pay less and have better access to the bond markets than sick ones, and the restructuring of one city is a lot less likely to have contagion effects on other cities in those states than people in the bond market tend to believe.

I just don’t find these kinds of arguments compelling. For instance, Greece is restructuring its bond markets severely right now – the bond markets have not shut down in Europe.

- Finally, Newt Gingrich and Rick Santorum would like the media and academia a lot more, if every interaction between media and academics covered the details as clearly and concisely as this interview does.

November 17, 2011

Balanced Budget Amendment Coming up For a Vote in Congress

Part of the deal made earlier this year to increase the Federal debt-ceiling included taking votes in both the House and the Senate by December 31 on a balanced budget Constitutional amendment. The House is expected to take its vote by tomorrow. The main provisions of the the version of the amendment expected to be considered are...

- A requirement that the President submit an annual balanced budget to Congress.

- A 3/5 vote requirement, to spend more in outlays than is taken in and receipts in any given year (with borrowed money not counted as "receipts", nor repayment of debt principal counted as an outlay).

- A 3/5 vote requirement, to raise the debt ceiling.

- A requirement that any bill to raise revenue be approved by a rollcall vote.

Rhode Island residents may be particularly interested in the differences, which are not major, between the current proposal and the balanced budget amendment that Senator Claiborne Pell voted in favor of in 1986…

- In the current version, votes to raise the debt ceiling or to deficit spend in a given year must be by roll-call.

- The exemption of borrowed money and repayment of debt principal from receipts and outlays wasn't in the 1986 version.

- The 1986 version expressly allowed the President to submit an alternate budget where outlays exceeded receipts, in addition the balanced budget.

- The 1986 version allowed balanced-budget requirements to be waived "for any fiscal year in which a declaration of war is in effect". The current version extends that to any year where the U.S. is "engaged in military conflict".

Despite the fact that this is a very mild version of a Constitutional-level budget balancing process, prepare to hear arguments from the fiscally-insane wing of the Democratic party that boil down to the idea that the Federal government cannot possibly function if the President uses a part of the Federal bureaucracy at his or her disposal to consider how to balance the budget, and that it's unreasonable to require a 3/5 vote of Congress when the government wants to spend more than it takes in.

November 7, 2011

Claiborne Pell Was a Fiscal Extremist, According to Today's Democrats -- He Supported a Balanced Budget Constitutional Amendment

In September, Rhode Island State Democratic Chairman Edwin Pacheco staked his party to an aggressive stand against adding a balanced budget amendment to the United States Constitution, characterizing such an amendment in an official press release as "extreme economic policy". But support for Federal spending-with-no-ending has not always been the singularly dominant position amongst Rhode Island's Democratic leaders that it is today. At a previous time when the Federal budget deficit had grown to unprecedented levels, at least one prominent RI Democrat gave his unambiguous support to a balanced budget constitutional amendment, in a year when it had a realistic chance of passage. That Democratic leader was United States Senator Claiborne Pell.

In 1982, Senator Pell voted against a balanced-budget amendment that passed the Senate by a vote of 69-31. (The amendment later failed to pass in the House).

By 1986, Senator Pell had changed his position and voted in favor of sending a balanced-budget amendment to the states for ratification. The amendment lost by a single vote, 66-34 (2/3 required for passage). The amendment that Senator Pell voted for -- and that the present chairman of the RI Democratic Party would presumably find "extreme" -- read...

SECTION 1. Total outlays of the United States for any fiscal year shall not exceed total receipts to the United States for that year, unless three-fifths of the whole number of both houses of Congress shall provide for a specific excess of outlays over receipts. The public debt of the United States shall not be increased to fund any excess of outlays over receipts for any fiscal year, unless three-fifths of the whole number of both houses of Congress shall provide, by law, for such an increase.In 1992, Senator Pell reiterated his support for adding a balanced budget amendment to the US Constitution, voting in favor of a non-binding sense-of-the-Senate resolution calling for its passage.SECTION 2. Any bill to increase revenue shall become law only if approved by a majority of the whole number of both Houses of Congress by rollcall vote.

SECTION 3. Prior to each fiscal year, the President shall transmit to the Congress a proposed budget for the United States Government for that fiscal year in which total outlays are not greater than total receipts. The President may also recommend an alternative budget in which total outlays exceed total receipts, which shall be accompanied by a detailed explanation of the need for such excess.

SECTION 4. The Congress may waive the provisions of this article for any fiscal year in which a declaration of war is in effect.

SECTION 5. The Congress shall enforce and implement this article by appropriate legislation.

SECTION 6. This article shall take effect for the fiscal year 1991 or for the second fiscal year beginning after its ratification, whichever is later.

By 1994, Senator Pell had changed positions once again and voted against two separate versions of a balanced budget amendment offered that year. During the floor debate in 1994, the Senator explained how his thinking had evolved over the preceding decade. Here is an excerpt, from the C-SPAN archives...

The intensity of the debate on the balanced budget amendment--and to a degree my own reaction to it--varies in proportion to the magnitude of deficits in the Federal budget over the last 12 years...Today, annual deficits run-up by the Federal government are much larger than the figure of $221 billion cited by Senator Pell in his explanation of his vote in favor of the 1986 balanced budget amendment. 2011 will be the third year in a row where the Federal deficit exceeds $1 trillion dollars, with no return to 1986 levels anticipated (in inflation adjusted dollars) in the next five years projected by the Office of Management and Budget.[In 1986] we were 2 years into the second Reagan administration and deep into a period of institutional deadlock between an executive branch that would not agree to fund programs and a legislative branch that often was not disposed to cut them. The deficit that year had risen to $221 billion.

The Senate that year narrowly failed to approve a balanced budget amendment, notwithstanding the fact that many of us--myself included again--this time felt that the institutional deadlock was approaching such drastic proportions that a constitutional solution might be the only way out of our dilemma...

Then, in 1992, things began to change for the better....As a percentage of gross domestic product, the fiscal year 1995 deficit is projected at 2.5 percent, down from 3.5 percent for fiscal year 1994. And it is expected to stabilize at 2.3 percent for fiscal year 1996-99. This is a significant figure because it shows that the deficit is very small relative to overall economic activity and the economy thus has substantial capacity to absorb the effects of deficit spending, albeit at levels which for other reasons certainly must be reduced.

In 1994, Senator Pell believed that the projected lowering of annual deficits to 2.3% of GDP made a balanced budget amendment unnecessary. Today, deficits are much larger than 2.3% of GDP and are larger as a percentage of GDP than they were when Senator Pell voted to send a balanced budget amendment to the states. 1986 had been the 3rd year out of 4 that the Federal deficit exceeded 5% of GDP (and in the 4th of those years, it was 4.8%). 2012 will be the fourth consecutive year that the deficit exceeds 7% of GDP (though OMB does project that it will be down to 3.3% of GDP by 2016 -- if you believe that the economy is going to grow by 23% while the percentage of revenue collected in Federal taxes jumps from 15% to 19% between 2010 and 2016).

Senator Pell thought that "institutional deadlock" was a problem in government during part of his tenure in office. This, at least, is something in common with current Rhode Island Democrats. In August, Rhode Island First District Congressman David Cicilline sent out a fundraising letter explaining his vote to raise the Federal debt ceiling as a response to "partisan gridlock". The difference, of course, is that Senator Pell believed that institutional deadlock made it necessary to strengthen constraints on Federal spending, while Congressman Cicilline believes that partisan gridlock justifies autopilot spending increases and unrestrained Federal borrowing -- and contemporary Democratic leaders like Edwin Pacheco believe that the kind of serious consideration Claiborne Pell gave to balancing the Federal budget is "extreme".

October 24, 2011

Walter Russell Mead on Rhode Island as Athens on the Pawtuxet

You could pick almost any combination of paragraphs from today's post by Walter Russell Mead at the American Interest and come up with an insightful excerpt that describes Rhode Island's problems. Here are the 3 1/2 I will choose...

Because Rhode Island listened to timeserving blue politicians too long, and union leaders and public sector workers lost their grip on any mathematical realities beyond the numbers at the ballot box, the pension system grew more and more out of control. State and local governments lurched into a crisis. Vote yourself a raise, vote yourself a pension: why not...Needless to say, read the whole thing.Let’s be crystal clear about this. To tell a 50 year old pretty lies about the soundness of a pension plan is one of the most wicked and irresponsible things you can do without actually shedding blood; people who believe these phony promises will not make the extra savings, work the extra years or otherwise take steps to protect themselves until it is too late. Telling those pretty lies is exactly what Rhode Island’s establishment has been doing for some time; it is what Ostrich Party legislators, trade unionists, journalists and governors are still doing across much of the country.

Reasonable reforms could have made things much less painful, but the unions typically threaten to destroy the careers of any politician who tampers with the pension system until the truck actually starts falling over the cliff...

Polarizing politics and demonizing state and local government workers is not a good idea. It is unfair for one thing; it is bad politics for another. Toxic blue model legacy costs are the problem: rigidly bureaucratic government structures, unrealistic costs, years of underfunded pension plans, regulations that choke growth and initiative, outdated progressive ideas about how change works — these are the roots of our problems, not the middle school teacher down the street or the retired post office worker living modestly on a pension that may be underfunded but is hardly a bonanza...

October 10, 2011

Even if it's Amazing, It's not fair, so I hate everything

Trying to figure out this Occupy thing? Right now, this seems to explain it the best (h/t):

Remember this bit by Louis CK (thanks for reminding me, Will)?

Protest song!

...a sultan and student both have iPhone 4s...it's not fair

Overall, much of the logic seems to go something like this (h/t):

ADDENDUM: I put this is all under our "On a lighter note...." category because there is humor in the unknowns surrounding the Occupy movement. Still, there are serious questions that haven't been answered.

Now, a movement that started with no concrete goals as a simple protest of power must decide what to do with some power of its own. Can a leaderless group that relies on consensus find a way for so many people to agree on what comes next? Can it offer not only objections but also solutions? Can a radical protest evolve into a mainstream movement for change?Unfortunately, from what I have heard of the solutions, they roughly approximate the tongue-in-cheek poster above. In writing about the recent passing of Steve Jobs, Kevin Williamson illustrated that there is a dichotomy:

The beauty of capitalism — the beauty of the iPhone world as opposed to the world of politics — is that...[w]hatever drove Jobs, it drove him to create superior products, better stuff at better prices. Profits are not deductions from the sum of the public good, but the real measure of the social value a firm creates. Those who talk about the horror of putting profits over people make no sense at all. The phrase is without intellectual content. Perhaps you do not think that Apple, or Goldman Sachs, or a professional sports enterprise, or an Internet pornographer actually creates much social value; but markets are very democratic — everybody gets to decide for himself what he values. That is not the final answer to every question, because economic answers can satisfy only economic questions. But the range of questions requiring economic answers is very broad.I was down at the Occupy Wall Street protest today, and never has the divide between the iPhone world and the politics world been so clear: I saw a bunch of people very well-served by their computers and telephones (very often Apple products) but undeniably shortchanged by our government-run cartel education system. And the tragedy for them — and for us — is that they will spend their energy trying to expand the sphere of the ineffective, hidebound, rent-seeking, unproductive political world, giving the Barney Franks and Tom DeLays an even stronger whip hand over the Steve Jobses and Henry Fords. And they — and we — will be poorer for it.

And to the kids camped out down on Wall Street: Look at the phone in your hand. Look at the rat-infested subway. Visit the Apple Store on Fifth Avenue, then visit a housing project in the South Bronx. Which world do you want to live in?

September 10, 2011

(Non)Funding of the American Jobs Act: "Paid For" Doesn't Mean Someone Else Will Find the Cuts!

Usually, when Democrats on the national level propose something that is misguided, irresponsible, stupid or - worst of all - presuming of stupidity on the listener's part, it goes in one ear and out the other. As this item from the President's speech Thursday night is all of the above in truckloads, however, there simply isn't room to let it pass.

And here's the other thing I want the American people to know: the American Jobs Act will not add to the deficit. It will be paid for. And here's how:The agreement we passed in July will cut government spending by about a trillion dollars over the next ten years. It also charges this Congress to come up with an additional $1.5 trillion in savings by Christmas. Tonight, I'm asking you to increase that amount so that it covers the full cost of the American Jobs Act.

So it's funded not because the President found a new "revenue" source or because he himself made room for it in the budget by identifying cuts. It's funded because he assigned someone else - i.e., Congress - the task of making the requisite budget cuts???

He goes on to say,

And a week from Monday, I'll be releasing a more ambitious deficit plan -– a plan that will not only cover the cost of this jobs bill, but stabilize our debt in the long run.

Again, absolutely no specifics at this point. But you go ahead, Congress, and identify half a trillion in budget cuts for my initiative. That way, you can get the political blame for those cuts and I'll get the praise when the initiative is implemented.

This is not the proposing of responsible policy or the sharing of a vision. It's the exposition of a fantasy, pure and simple. No amount of Presidential spam

After the president’s jobs speech before Congress Thursday night, his staff sent out 39 e-mails to reporters, each declaring that yet another Obama ally “backs the American Jobs Act,” as the subject lines boasted.The e-mails came within a 1-hour, 5-minute period between 8:32 p.m. and 9:37 p.m. That’s an average of one every minute and 40 seconds.

can make it otherwise.

September 7, 2011

Who Pays for Past Mistakes

Generational warfare: It's bound to happen here in Rhode Island with the pension crisis. It's also happening nationally on the budget deficit debate with the new Super Congressional panel set to convene. Education Policy wonk Rick Hess offers his perspective:

You're either with the kids or with those rushing to the ramparts to defend retiree entitlements. So, which is it?Past or future? Which will it be? He provides an important breakdown of we pay for current Medicare spending:Consider the President's vague calls last week to spend billions more on school construction and preserving school staffing levels (which would've been more compelling if he had offered any inkling as to how we might pay for it). Obama finds himself unable to do more than offer marginal, dead-on-arrival programs because the feds have spent more than half the budget just mailing checks to retirees, covering health care bills, and paying interest on the accumulated debt. Everything else—schools, financial aid, the FBI, defense, transportation, the environment, NASA, foreign aid, you name it—has to make do with what's left.

As Julia Isaacs at the Brookings Institution has pointed out, the federal government now spends about $7 on seniors for every $1 it spends on children....Do we really think it's a good idea to spend half of all non-interest spending on making retirement ever more comfy?

[T]oday's retirees have contributed taxes that amount to less than half their Medicare outlays. Today's Medicare payroll tax doesn't fund Medicare--it funds only Part A (hospital expenses). Premiums cover just 25 percent of Part B (doctor treatments and visits). And premiums for Bush's Medicare drug program (Part D) cover just 10 percent of the cost. The rest of the hundreds of billions in outlays for these programs is vacuumed out of general revenue. (See here for a good breakdown on Medicare funding.)And Social Security:

Social Security has the government reflexively spending hundreds of billions to mail out monthly checks to the wealthiest segment of the population, without an ounce of thought as to whether that's the best use of borrowed funds (the famed Social Security "trust fund" being, you know, nonexistent). The Social Security Administration reports that more than 20 percent of those 65+ have incomes over $65,000 a year. In a nation where median household income is in the $40,000s, is it really radical to rethink how much we mail to these households every month?As for taxes:

Toss in all of the tax deductions that President Obama called for eliminating this summer, including the corporate jet deal, and you address another $400 billion over 10 years, or less than 2 percent of the shortfall. So, just keeping the deficit from exploding will involve all those taxes and trillions more in cuts. Those demanding substantial new spending then need to raise hundreds of billions beyond that, through additional cuts or tax increases....Even with hefty tax increases, protecting existing entitlements ensures that we won't have much available for schools, colleges, or anything else.He urges education advocates to step up to the plate and take on the AARP and similar groups so that more money can go towards kids and education.

In short, it's possible to get our house in order, free up dollars for schooling, and shift dollars towards youth. But doing so requires facing down the massive, intimidating seniors' lobby.Hess' bailiwick is education and his goal is to increase funding for it. Regardless of whether you agree or disagree with Hess' priorities, his argument helps to lay out the choice that needs to be made: should the people who benefited or made the mistakes in the past be held most accountable for those mistakes? Or should their kids and grandkids?Shared sacrifice involves asking Baby Boomers and retirees to step up and, you know, sacrifice. It doesn't mean holding harmless the generations who voted themselves free stuff through the good times and doesn't rely almost entirely on raising taxes and curtailing benefits for the under-40 set.

August 11, 2011

The Protest Against the Debt Ceiling Deal

Yesterday, MoveOn.org and several like-minded local groups held a protest at the statehouse. According to Philip Marcelo of the Projo, the theme was opposition to the debt-ceiling deal signed into law last week.

Immediately following the Tax Day Tea Party rally this past April, commentary was offered, in this and other forums, that not enough people had attended for the event or its message to be considered significant. (The commentary was usually offered from people who wouldn't agree with the Tea Party's message no matter how many people attended, but I digress.)

For purposes of comparison, I stopped by yesterday's protest, to compare crowd sizes. Here's the debt ceiling protest...

The photograph above was taken at roughly the same angle as this photo from this year's April 15 rally...

But back to yesterday (both literally as well as metaphorically, in terms of policies being advocated). Let's move in a little closer...

...and a little closer still...

...to get a more detailed picture of the "crowd".

One other note: At the time I arrived, one of the protesters was reading a message from First District Congressman David Cicilline, written specifically for this event. As the 2012 campaign progresses, it will be interesting to see if comparable (or larger) size events receive similar personal attention from Congressman Cicilline, or if organizations arguing against major Federal spending reforms hold a special place in the Congressman's heart.

August 10, 2011

Majority of Americans Understand What Government "Cuts" Really Mean

I've complained about the "cuts" game played by the government. I'm happy to learn that most people get it:

Congress and presidents have been playing the “spending cuts” game for years, but most voters know what they’re really talking about.Why does the government call these reductions cuts? (Hey, I know you know, but I never tire of this explanation!)Sixty-two percent (62%) of Likely U.S. Voters understand that when Congress mentions future spending cuts, they’re really saying the growth in government spending will be less than planned. A new Rasmussen Reports national telephone survey finds that just 19% think it means spending next year will be lower than this year’s. Twenty percent (20%) aren’t sure which is right....

Interestingly, those who are pushing hardest for government spending cuts are the ones who are most aware of what those cuts really mean. Two-out-of-three Republicans and voters not affiliated with either party – 67% - recognize that congressional promises of spending cuts mean the growth of spending will be less than planned, but just 51% of Democrats share that awareness.

The federal government has been using a process known as Current Services Budgeting since the 1970s to report spending changes. That means the “baseline” for spending is assumed to include all the spending growth that is already built into the federal budget. Much of that growth comes from what the Congressional offices call “uncontrollable spending,” which includes entitlement programs and accounts for the vast majority of all federal spending.Yup, to them and the mainstream media it's a cut.To see the impact of Current Services Budgeting, assume that government is projected to grow by 10% from one-year to the next. If that spending grows by just 5%, Congressional scorekeeping would consider that to be a 5% cut. However, in the real world, an increase in spending by 5% is an increase in spending no matter how you spin it. To be precise, the official numbers would consider that to be a reduction in “current services” but politicians have long since lost that distinction.

August 6, 2011

What Was Standard and Poor's Expecting to Happen?

This is from Page 3 of the official statement from Standard and Poor's on their downgrade of the US credit rating...

Despite this year's wide-ranging debate, in our view, the differences between political parties have proven to be extraordinarily difficult to bridge, and, as we see it, the resulting agreement fell well short of the comprehensive fiscal consolidation program that some proponents had envisaged until quite recently.I suppose you could say that the Republicans had the Ryan plan and the Democrats had the "Cicilline plan" (borrow today and let somebody else worry about it tomorrow), but the Ryan plan never got close to passing in its original form and the "Cicilline plan" is hardly comprehensive. Ultimately, any change away from business as usual brought about by the debt-ceiling and budget deal will be a result of, not in spite of, the Tea Party standing their ground during the sometimes contentious legislative process.

Over the past several years, I've heard the opinion offered in multiple discussions that we will know that the government has become serious about fiscal reform when it creates the kind of commission used to decide on military base closings to develop a plan. The distinctive feature of the base-closing process is that the work of the commission must be approved or rejected in its entirety; this week's budget-deal was a full step in that direction, with its creation of the "super-committee" to create an unamendable deficit reduction program (along with an enforcement mechanism of automatic budget cuts in many Federal departments if the committee fails to act, or if a balanced budget is not passed by both Houses of Congress).

Obviously, the base-commission structure wasn't any factor in the Standard and Poor's analysis. So what exactly is in the "comprehensive fiscal consolidation program" that the S&P analysts thought Congress fell short of?

August 3, 2011

How Surprising is it that the Dow Dropped After the Debt Ceiling Deal?

I saw a headline from a CNN newscast from last evening that read "Dow Drops Despite Debt Deal". With the disclaimer that you don't want to attribute too much significance to a single day's movement in the stock market, I don’t see the drop as paradoxical or even random.

The first chapter of any book on technical finance will tell you that stocks and bonds move in opposite directions. When "the market" feels investment opportunities in businesses are likely to pay off, money moves towards stocks and away from the assumed safety of bonds; when "the market" feels there are fewer good business investment opportunities, money moves towards bonds.

The down-to-the-wire debt ceiling negotiations jumbled the traditional logic and created a perception that bonds weren't as safe as usual. The eventual deal mitigated the worries.

So, if I may borrow Justin's juxtaposition from a previous post, it would not be surprising if a restoration of confidence in the ability of the Federal government to make its debt payments on time led “the markets” to wager that investing in the government's ability to tax is once again a better bet than actual investment in productive enterprise.

Who says that markets are rational all of the time!

Beating the "Budget Cuts" Horse Unicorn

I know I've beaten and flayed this particular horse unicorn (a unicorn is a mythical creature, just like actual government "cuts"), but I continue to stress that there are no "cuts" in the recent deficit deal because it undermines the hyperbolic sturm und drang being propagated by liberals like Froma Harrop who are calling Tea Partiers "terrorists" for supposedly "holding America hostage" while demanding "cuts": Again, and slowly, there are no "cuts" to the budget in the deficit ceiling deal.

There is something you should know about the deal to cut federal spending that President Obama signed into law on Tuesday: It does not actually reduce federal spending.That from the NY Times. Reason's Jacob Sullum gives a bit more detail:Indeed, both the government and its debts will continue to grow faster than the American economy, primarily because the new law does not address federal spending on health care.

That is the reason that the ratings agency Standard & Poor’s and its rivals still are threatening to remove the United States from their lists of risk-free borrowers, although the other agencies, Moody’s and Fitch, both said Tuesday that they would watch and wait for now.

The debt deal, which authorizes the federal government to borrow another $2.1 trillion on top of the $14.3 trillion it already owes, supposedly includes "$2.5 trillion in cuts." But as Sen. Rand Paul (R-Ky.) emphasizes, those are cuts from a projected baseline in which the national debt grows by $10 trillion during the next decade, which means "the BEST case scenario is still $7 trillion more in debt over the next 10 years."Imagine the rhetoric if Tea Partiers were able to enact real cuts? Maybe we'll find out after 2012.Paul also notes that the vast majority of the "cuts" are not scheduled to take effect for years, raising serious doubts about whether they will happen at all. "Why do we believe that the goal of $2.5 trillion over 10 years…will EVER be met," he asks, "if the first two years' cuts are $20 billion and $50 billion?"

Well, you might say, the debt deal is only the first step. But even at their boldest, House Republicans do not envision a federal government any smaller than it is now. Under the supposedly radical budget plan approved by the House in April, Cato Institute budget analyst Chris Edwards calculates, federal spending would rise by 34 percent during the next decade, compared to the 55 percent preferred by Obama. The budget would not be balanced until 2030, while the role of the federal government would be essentially unchanged.

August 1, 2011

Debt Ceiling Deal Passes House

The debt ceiling and budget deal has passed the House, with Congressmen James Langevin and David Cicilline both voting in favor.

Keith Hennessy has a good summary of what's contaned in the deal, available here (h/t Instapundit).

July 31, 2011

Is this the Debt Ceiling Deal That Will be in the News Tomorrow?

Kathryn Jean Lopez of National Review Online has posted an outline of a debt ceiling and budget process deal that Speaker of the House John Boehner sent to the Republican caucus this evening.

History Will Begin to be Made this Week

This is very likely going to be a memorable week in the history of self-government and public finance.

In addition to the Federal debt-ceiling issue which needs to be resolved by Tuesday in order for the Federal government to be able to keep paying everything it owes without resorting to various less-than-scrupulous financial gimmicks, the receiver for Central Falls may make an announcement as early as tomorrow that he is filing for bankruptcy. As Philip Marcelo wrote in today's Projo...

The square-mile city would be entering uncharted waters as federal municipal bankruptcy has been rarely tested nationally.Central Falls is not sui generis; it is an advanced case of a situation faced by many cities and towns across the United States, and what happens with CF is going to contribute very visibly to a body of legal, policy and political knowledge about what to do and/or what to avoid when twenty-first century communities run out of money needed to pay for decisions made over preceding decades.

But the most important thing to keep in mind is that nothing ends this week. The reckoning (to use Matt Allen's word) of the fiscal crisis created by the political and social changes of the past 45 to 80 years, depending upon if you want to place the beginning of the problem with the New Deal or the Great Society or somewhere in between, is just beginning and what our society will look like as a result, for better or for worse, will be decided more by the reaction to this week's decisions than by the decisions themselves.

Finally, one symptom visible in Central Falls of the problem that is nationwide is captured beautifully by the quote from freshman state Rep. James McLaughlin in the Projo's CF story...

"They’re going to file for bankruptcy," said state Rep. James N. McLaughlin, a Democrat who represents a portion of the city and is opposed to [filing for bankruptcy]. "All avenues have not been exhausted. It is a rush because they do not have any money."If our politics keeps producing a large number of elected officials who believe that just because we have no money doesn't mean we're bankrupt, we're basically doomed.

July 28, 2011

No Debt Ceiling Vote Tonight

Various sources tweeting from Captiol Hill are saying there will be no debt ceiling vote tonight.

Robert Costa from National Review Online: Top GOP member confirms no vote tonight, still working on whip count and changes. Weary mood among leadership. Not lost, but no slam dunkHowever, there's some kind of activity with the House Rules committee scheduled for later tonight...

Chad Pergram from Fox News: Rules Committee will convene around 11 pm, per sr. House source.UPDATE:

An apparent correction of the above, the House Rules committee will meet at 11:00 am tomorrow, concerning the debt ceiling bill, not at 11:00 pm tonight...

Chad Pergram of Fox News: Rules to meet at 11 am...to give them the ability to write a new rule tomorrow to govern a tweaked bill. No idea what tweaks are.

July 22, 2011

Understanding the Debt Ceiling

0. Just like any other organization, the Federal Government is subject to laws of economics, probability and mathematics that it can’t change.

1. Every organization, including the Federal Government has a cash flow, related to but different from an annual summation of revenues and expenditures. For example, your local bridge club may have $600 in revenues and $600 in expenditures for the year, but if the revenue comes in at a rate of $50 per month and $300 has to be paid for the big event in February, the bridge club needs to find a way to get extra revenue up front.

2. Of course, if you have $600 in revenues and $800 in expenses each year, your organization has more than just a cash flow problem; it has a structural imbalance in its budget. Eventually, the organization will run out of money to pay for anything. If no one is watching carefully, the structural imbalance will show up as a cash-flow problem in the bridge club’s day-to-day operations, even though the problem is bigger than just the cash-flow issue.

3. On August 2, 2011, according to all reasonable estimates, the Federal Government’s cash flow will go negative, i.e. there won’t be enough money in the U.S. Treasury to cover the government’s debts. A group called the Bipartisan Policy Center, which was founded by a respectable mix of graybeards and who seem to be doing reliable and understandable work, has published a day-by-day analysis by major line item of what is expected to come in and what is scheduled to be paid out in August.

4. The anticipated August cash-flow crunch does not mean that the Federal government will immediately default on its loans. Working from BPC numbers, the government is expected to have $172.4 billion in cash available in August after the 2nd, while interest payments on debt will amount to about $29 billion. In total, the Federal government is expected to have enough money to pay only 56% of what it owes in August. Raising the debt-ceiling would allow the government to borrow the money to cover the immediate cash-flow problem. For how long would be determined by how high the limit is raised.

5. If the debt ceiling is not raised, we are into uncharted territory. Does the Federal government pay off bills in some kind of "order that they come in" until the money runs out, or does Congress or the executive branch make decisions about who gets paid?

6. If you examine the historical numbers in the bipartisan report (pg. 13), you see that the cash-flow deficit (minus borrowed or other up-front money) in this particular August is not significantly different from previous recent Augusts. This means that if the only thing that happens in the next couple of weeks is a raising of the debt ceiling, government will just keep paying out more than its takes in, until the same cash-crunch as a symptom of a structural imbalance recurs, but with an even larger debt. Borrowing forever and never paying it off cannot be infinitely sustained, even by the government; see point 0 as to why. Raising the debt ceiling in isolation, aka the David Cicilline Providence plan of keep-borrowing-then-run-away, is not a viable solution.

7. According to the BPC’s numbers and various news reports, the $111 billion dollars in spending cuts in the “cut, cap and balance” plan passed by the House (but rejected today by the Senate) – even if it all could be implemented in a single month, which is doubtful -- would patch less than one month of the government’s current cash flow problem (score one for commenter jgardner03). However, the fact that big spending cuts would be needed to bring the budget into balance is not a reason to say nothing should be cut.

8. Here’s the outline of a possible solution I would tend towards at the moment: Raise the debt ceiling enough to cover the next six-months of cash flow for the government, in conjunction with the $111 billion “cut” in spending and implementation of the GDP-based spending “cap” passed by the House. Then, over the next six months, Congress would work on a program to start hitting the spending caps, and to pass a balanced budget amendment. No further increase in the debt ceiling would be on the table, unless one or maybe both of the preceding were passed by Congress.

July 20, 2011

What is Cut, Cap and Balance?

The Republican "Cut, Cap and Balance" plan for addressing the tendency of government budgets to increase towards infinity passed the House yesterday. President Obama has said he would veto at least an earlier version, and Rhode Island Representatives James Langevin and David Cicilline both voted against it.

Title I of the bill is the cut, which would be an immediate cut in the 2012 Federal spending total Various news reports place the size of the cut at $111 billion. The direct language in the bill says that spending on Social Security, Medicare, veterans’ benefits, net interest on the debt would be exempt from cuts, and spending on the global war on terrorism would have its own cap.

In March, Brian Riedl of the Heritage Foundation, using numbers from the Office of Management and Budget, estimated a total of $3.7 trillion in outlays to be made by the Federal government in 2012 (including interest on the debt). According to his numbers, the exempted programs account for about $1.8 trillion, which means that the $111 billion in cuts will have to come from a total of about $1.9 trillion from the remaining programs, a cut of about 6%.

Title II is the cap: An annual federal spending cap, as a percetange of total GDP, would be phased in. The schedule would be...

21.7 percent for fiscal year 2013;If I understand blogger and former director of the President's National Economic Council Keith Hennessy correctly, the caps would be enforced by (almost) across-the board reductions in Federal spending needed to hit the targets, if an initial budget was submitted that exceeded them. It is "almost" across the board, because payments for military personnel accounts, TRICARE for Life, Medicare, military retirement, Social Security, veterans, and net interest would be exempt from the automatic reductions.

20.8 percent for fiscal year 2014;

20.2 percent for fiscal year 2015;

20.1 percent for fiscal year 2016;

19.9 percent for fiscal year 2017;

19.7 percent for fiscal year 2018;

19.9 percent for fiscal year 2019;

19.9 percent for fiscal year 2020;

19.9 percent for fiscal year 2021.

Title III is the balance: An increase in the debt-ceiling of the United States would be triggered by the passage of a balanced-budget constitutional amendment by both houses of Congress. (It would not become the law of the land, of course, until ratified by 3/4ths of state legislatures after that).

Arguably, the "balance" is a radical approach to the problem, at least in a procedural sense -- asking for a constitutional amendment to solve an immediate problem is a tall order. But that issue aside, what's radical about the "cutting" and "capping" provisions?

July 18, 2011

"Rhode Island's Rising Pension Tide": Some Questions for Gary Morse

At the conclusion of the Providence Republican City Committee's event on "Rhode Island Rising Pension Tide" last Thursday, I was able to ask presenter Gary Morse (no relation) a few questions about specific numbers and predictions for the future.

Question: I've heard the claim made the pensions are superior to 401(k)-type plans, because aggregating all of the money into one place allows for a higher rate of return. Is that true or not?

Q: Earlier in your talk, you mentioned the lowering of the discount rate from 8.25% to 7.5%, and some skepticism about 7.5% being accurate...

Gary Morse: "...if you had invested in a balanced portfolio, when you came in as a teacher in 1980, you would have outperformed the investment rate that you got from the state..." Audio: 39 sec

Q: Knowing both the numbers as you do and being aware of the politics of the situation, if there was one thing, one message that you could give to everyone who is participating in this debate and make sure that they really knew, what would that be?

GM: "...the State Treasurer's office polled their investment advisors, and they said there's only about a 42.5% chance that they're going to make 7.5%..." Audio: 35 sec

Q: What is a reasonable expectation that people should have about the planned legislative session fall where pension issues are supposed to be addressed?

GM: "The message is, we needed an inspector general..." Audio: 1m 4 sec

GM: "I don't think we are going to see anything substantive come out of the General Assembly this fall". Audio: 34 sec

July 16, 2011

Debt Ceiling Stand-Off: What Does Compromise Look Like When We Already Borrow 43 Cents of Every Federal Dollar Spent?

This staggering item stands out from Mark Steyn's (characteristically excellent) column of today.

When the 44th president took office, he made a decision that it was time for the already unsustainable levels of government spending finally to break the bounds of reality and frolic and gambol in the magical fairy kingdom of Spendaholica: This year, the federal government borrows 43 cents of every dollar it spends, a ratio that is unprecedented.

What an absurdly irresponsible and dangerous position this and the prior Congress and President have placed us in.

President Obama, around the same time he made it clear that he would cut social security checks for seniors and the infirm before he would cut funding for high speed rail (and other boondoggles) or welfare benefits for the healthy, called for compromise.

Setting aside that legislative "compromises" got us to this point, how can there be talk of compromise when 43% of your annual operating funds are borrowed? Doesn't any kind of "compromise" still leave us in the area of unsustainable spending?

July 15, 2011

"Rhode Island's Rising Pension Tide": The History that Makes the Future

At a forum sponsored last evening by the Providence Republican City Committee, Gary Morse (no relation), the primary advisor to 2010 Republican Gubernatorial candidate John Robitaille on the subject of pension issues, delivered a talk titled "Rhode Island's Rising Pension Tide". The Providence Republicans promised that this would be a non-partisan forum, and Mr. Morse delivered.

Mr. Morse used a significant portion of his speaking time to go into serious detail about the evolution of pension law and of pension systems in the US, and the resulting constraints that will shape the possible choices as we move forward...

1. The meaning of "the discount rate" and its value. Audio: 1m 11 sec The troubles with the discount rate, including spiking. Audio: 1m 54 sec How much does spiking cost the taxpayers?

Audio: 32 sec 2. The changes to pension law and pension practice that occurred in 1991 and 2006.

(1) Audio: 1m 19 sec; (2) Audio: 1m 56 sec; (3) Audio: 2m 58 sec

3. How what has happened in a place called Pritchard, Alabama could impact Chapter 9 bankruptcy proceedings in a place called Central Falls, Rhode Island.

Audio: 2m 45 sec 4. Some suggested reading, if you're interested in how the courts might decide the pending Council 94 lawsuit.

Audio: 42 sec 5. The role that debt played in the Suez crisis of 1956, and its parallels to today.

Audio: 1m 45 sec 6. A not-very-rosy prediction for everyone's future. Audio: 1m 32 sec

July 14, 2011

Liveblogging “Rhode Island’s Rising Pension Tide”.

Good evening. I will be liveblogging the presentation being made by Gary Morse (no relation) this evening on the subject of Rhode Island’s pension problems, sponsored by the Providence City Republican Committee…

Gary Morse speaking:

Rhode Island is number 50 in unfunded pension liability.

Mr. Morse wants to dispel the notion of the greedy state worker and the greedy teacher.

Retirements pre-1990 in the private sector were much better than in the public sector.

In 1985, Bank of America created a cash-balance pension plan. The structure, however, violated age discrimination laws.

As a result, one sentence was added to Federal law, making BoA’s practice legal. After this law was passed, companies began replacing their defined benefit pension plans with cash-balance plans.

The big money was in rolling people from defined benefit plans into the new cash benefit structure. People were told they would get their pensions, if they made it to age 65 -- and then bunches of them get laid off in their 50s.

In 2006, the Federal government allowed anyone to convert a pension plan into a cash-balance plan. Benefits are not based on the final three years, but what you’ve earned over your entire career.

Still, up until 2007, public private pensions were clearly better than public sector deals. (Backfill: The correction here was a pure typo)

Actuaries are overlooking the effects of end of career spiking in their calculations.

The discount rate will go even lower than 7.5%.

Spiking of 10% in the final years leads to a 25% bigger taxpayer contribution.

(The MERS plan disallows spiking, by the way. That’s why it is in better shape than other pension plans).

Mr. Morse discusses Central Falls.

Based on the case of Pritchard, Alabama, it is possible that CF pensioners could not receive their checks for a year or more. In CF there is almost no money in the pension fund. A judge can terminate their payments, after they declare chapter 9.

What will the headlines read, if retirees have their pensions terminated? Will the GA step up and find the money for them? What ever the answer is, CF will likely be the precedent.

I’m pausing, while Mr. Morse is taking various and sundry questions…

Pension liability is 10% of GDP GDP per-capita in Rhode Island. The US average is 4%. (Backfill: Thanks to the speaker for pointing out my error here)

So what can we do about this problem?

If Rhode Island had maintained a basic pension system without the extra perks, this problem would not have been created. The system needs to be stripped down to a basic pension plan.

End spiking.

We have to assume slow investment growth, and adjust the discount rate accordingly.

There isn’t enough money in the Rhode Island economy to carry our current debt load.

Mr. Morse is taking more questions from the audience. More detail to follow...

July 12, 2011

It's the cuts, stupid

It's tedious to follow the debt ceiling/budget deficit wrangling, I know. Around here, we have the ProJo trumpeting tax increases as the "obvious fix" and telling the Republicans "to do what grownups do" while explaining that "the health-care reform law passed last year would have begun to kick in its projected savings for the government" by 2015. Just trust Obama, right? After all, he's proposing $3 in cuts for every $1 in tax increases (or something like that). Really (and a second source)?

Sen. McConnell has been in talks with Obama and Democrats. We wanted to do something serious and big. Yesterday, he asked point blank how much the Biden-led deal would actually cut from next year's budget. Sen. McConnell has been in talks with Obama and Democrats. We wanted to do something serious and big. Yesterday, he asked point blank how much the Biden-led deal would actually cut from next year's budget. The answer he received was $2 Billion, and it's all smoke and mirrors. In exchange, [Democrats] want $1 Trillion in tax hikes. It's not the kind of deal we're at all interested in. We won't accept guaranteed tax hikes in exchange for fantasy future spending cuts. It's not going to happen. We're going to fight like hell to do what we've said we want: Real spending cuts and caps, a vote on a Balanced Budget Amendment, and real entitlement reform. ">The answer he received was $2 Billion, and it's all smoke and mirrors. In exchange, [Democrats] want $1 Trillion in tax hikes. It's not the kind of deal we're at all interested in. We won't accept guaranteed tax hikes in exchange for fantasy future spending cuts. It's not going to happen. We're going to fight like hell to do what we've said we want: Real spending cuts and caps, a vote on a Balanced Budget Amendment, and real entitlement reform.Got that? $1 trillion in tax hikes now and $2 billion in budget cuts. Yeah, seems fair.

July 5, 2011

Providence used as example of how "Compensation Monster [is] Devouring Cities"

Steve Malanga looks at the national problem of cities in over their heads (particularly because of pension promises) and uses Providence (and New Haven, CT) as examples:

Cities are also running out of fiscal alternatives to deal with their deficits. Like states...many cities have used one-shot revenue deals, hidden borrowing, and other gimmicks to bolster their finances. The weak economy has lasted so long, though, that these techniques have been exhausted. To balance its 2010 budget, for example, Providence, Rhode Island, borrowed some $48 million (using its fire stations and headquarters as collateral); it also drained most of its reserve fund, which shrank from $17 million to $2 million in just one year. Moody’s Investors Service and Fitch Ratings subsequently downgraded the city’s bond ratings by two notches, essentially ending its ability to use fiscal gimmicks. But Providence still faces a budget squeeze because its retiree costs amount to 50 percent of tax collections.Nationally, the rate of growth of such local expenditures outpaced state and federal:

Local governments also helped bring on their current budget nightmares by carelessly expanding hiring and wages in recent boom years. In the decade leading up to the 2008 financial crash, the number of workers for cities, towns, and schools increased 16 percent, even though the country’s overall population grew just 12.5 percent. Wages also increased, and, of course, the hiring frenzy made those pension obligations even worse. The result: over the same decade, the total in wages and benefits that public schools paid to teachers and noninstructional staff (to take one category of public-sector worker) jumped an amazing 72 percent, despite moderate increases in student enrollment.As Ted Nesi highlighted, albeit over a longer period, local government payrolls increased while state payrolls went down. Some argue that the cuts in state jobs have led to the increases at the local level. But, looking at Nesi's chart, it's obvious the local growth doesn't equate to the state reduction.

May 26, 2011

No Place Screws Up the Concept of Fiscal Responsibility Quite Like Rhode Island Does

The bill being heard today by the House Finance Committee that would give municipal bondholders a "first lien" on local government treasuries (H5376), introduced on behalf of the Rhode Island Department of Revenue and already passed by the Senate Finance committee (S0614), should not be passed into law. Peder Schaefer of the Rhode Island League of Cities and Towns, which has taken a position against the bill, relays a key rationale being advanced by its supporters, as offered at the Senate Finance hearing: "A bond lawyer retained by the Department of Revenue testified that the real reason for the bill was in the event of a Federal Bankruptcy in Central Falls. She testified that if this were to occur, bond holders would not have a first lien on city revenues. She believes that the language of the act would improve the credit quality of all municipal bonds in the state".

In other words, the Chafee administration Department of Revenue believes that a community should not be allowed to drastically restructure its finances to deal with a financial meltdown until the bondholders are taken care of. The bondholders come first, and then everyone else can fight over what's left.

But even those who don't believe that full-blown bankruptcy for Central Falls or any other Rhode Island community is likely should be troubled by this bill.

1. Allowing "first liens" on general tax-revenue does damage to the underpinnings of democratic governance. Tax revenue is taken from the income and/or wealth of taxpayers; revenue doesn't magically fall out of the sky, despite what some government officials might believe. To create a bondholder lien on general tax revenue is to create a bondholder lien on taxpayers, i.e. to grant one group of people long-term, legally enforceable claims on the incomes and wealth of another. This is less compatible with modern than with medieval concepts of government and property rights, and I don't think there's any case to be made that we will do any better than our ancestors did under a system where regular citizens can find a portion of their incomes automatically claimed by a class of people who assert their superior position in the order of things.

2. Consider possibile outcomes, short of Federal bankruptcy, in the case of Central Falls. Section 45-9 of RI law (already in place) gives a receiver the power to issue bonds on behalf of his municipality including the power to use them to fund a deficit or to fund pension obligations. (Regular municipal governments are barred from issuing bonds to cover a deficit; the current bill reinforces that a receiver is immune from this limitation). The receiver cannot break collectively bargained contracts, so union benefits are locked in. And if this bill is passed, bond-holding financiers will be locked in too -- which means that it's the people in-between who will absorb the entire burden of government's inability to rationally finance itself, as everyone else will have to be paid first, before regular citizens get anything from government. Except the bill, of course.

3. I know there is a group of people who believe that financial efficiency is the primary issue that needs to be addressed by government, and who aren't much concerned with the undemocratic system being installed for dealing with Rhode Island's financial mess (I think there may be more than a few of these folks in the Chafee administration). But even those who believe in nothing but the brutal efficiency of markets should be troubled by the imbalance created by this bill. If government writes into law that bondholders have a direct legal claim to money in the public treasury, then there is little to no risk of them not receiving their scheduled payments, and every bond covered by the law should be given the highest possible rating with lowest possible interest. Financiers who want to assert a legal claim over a portion of the tax levy and a right to take money through legal compulsion are not assuming true market risks, and should be paid accordingly.

In a special report put out last November, the Fitch Ratings service concurred with the idea that "first lien" bonds involve very limited risk, because people are required to pay whatever amount government demands of them...

Question: Given the strained finances of most state and local governments, and the likelihood of continued difficult times to come, why do Fitch’s ratings suggest confidence in the ability of most to meet their debt?The attitude reflected above, by the way, is why you should never trust the "financial efficiency is everything" crowd to run the government.Answer:...Other commonly issued municipal bonds are secured by a first lien on sales or income taxes, where there is little if any legal discretion for the taxpayer to choose not to remit the taxes owed to the government.

Once upon time, in the Western tradition of democracy and self-government, it was understood that government's ability to compel people to surrender a portion of the fruits of their labor was a critical reason for limiting government claims on the property of the citizenry and to err on the side of the taxpayer. Rhode Island is sadly leading the way in eroding this tradition, asserting instead that government power to compel payment of taxes is a valid reason for allowing groups of people favored by the political class to make near-permanent claims on the livelihoods of average taxpayers.

May 4, 2011

Looking More Closely at the Plan to Reverse Cuts to Higher Education

A Gina Macris story in today's Projo discusses funding for public higher education in the always-troubled Rhode Island state budget...

Governor Chafee’s budget would add a total of $10 million to higher education, stopping the decline in state support and sparing Community College of Rhode Island students tuition increases. But the system as a whole will still have to cut expenses, even with the tuition hikes at URI and RIC....and in a statement earlier this year, University of Rhode Island President David Dooley emphasized past cuts...

"As you all know (Tuesday) night was quite an occasion for higher education in Rhode Island,” Dooley said during a press conference called by the Governor at URI to discuss his plans to reverse years of heavy budget cuts to URI, Rhode Island College and the Community College of Rhode Island.However, despite the references to state budget cuts or expense cuts, the overall public higher education system in Rhode Island hasn't experienced anything resembling heavy budget cuts in recent years.

1. Total expenses for "Public Higher Education" in Rhode Island are listed in this year's gubernatorial budget document...

| Public Higher Education Total Expenditures | |

| FY 2009 Actual | $842,410,188 |

| FY 2010 Actual | $901,551,465 |

| FY 2011 Enacted | $937,802,389 |

| FY 2011 Revised | $996,080,552 |

| FY 2012 Recommended | $994,958,261 |

2. The $95 million dollar jump from FY2010 Actual to FY2011 Revised seems to include some Federal stimulus funding. Federal expenditures for public higher education are listed as...

| Public Higher Education Federal Funds | |

| FY 2009 Actual | $3,735,333 |

| FY 2010 Actual | $3,746,126 |

| FY 2011 Enacted | $15,004,667 |

| FY 2011 Revised | $32,657,457 |

| FY 2012 Recommended | $4,594,756 |

3. Though some of the stimulus funding might have gone towards capital costs, the portion of the RI public higher education budget classified as "operating expenditures" has not experienced any overall budget cuts, heavy or otherwise...

| Public Higher Education Operating Expenditures | |

| FY 2009 Actual | $777,838,168 |

| FY 2010 Actual | $838,415,178 |

| FY 2011 Enacted | $850,217,635 |

| FY 2011 Revised | $887,207,836 |

| FY 2012 Recommended | $926,649,575 |

4. Finally, it is interesting to contrast the increase in public college and university operating costs with the "other funds" figure from the revenue-side of the report, which in the case of public institutions of higher education, is mostly tuition. The first column below is operating expenditures, the second column is revenue from "other funds"...

| Public Higher Education Operating Expenditures | Public Higher Education Other Funds | |

| FY 2009 Actual | $777,838,168 | $667,142,742 |

| FY 2010 Actual | $838,415,178 | $735,958,261 |

| FY 2011 Enacted | $850,217,635 | $758,260,879 |

| FY 2011 Revised | $887,207,836 | $799,919,901 |

| FY 2012 Recommended | $926,649,575 | $816,021,529 |

The point is, as is the case in many areas of the Rhode Island budgets, that sources of growth in spending need to be identified and addressed at some point. Government funding of any program, no matter how worthwhile, cannot forever keep pace with faster-than-inflation growth in costs.

April 26, 2011

H'mm, What's Steve Laffey Up To?